The term ‘credit limit’ indicates the maximum amount that you can spend using your credit card within a specific given time. This limit undeniably plays a vital role in how you manage your finances.

Every credit card issued by a bank. And it comes with a predefined credit limit based on your income, credit history, and repayment capacity.

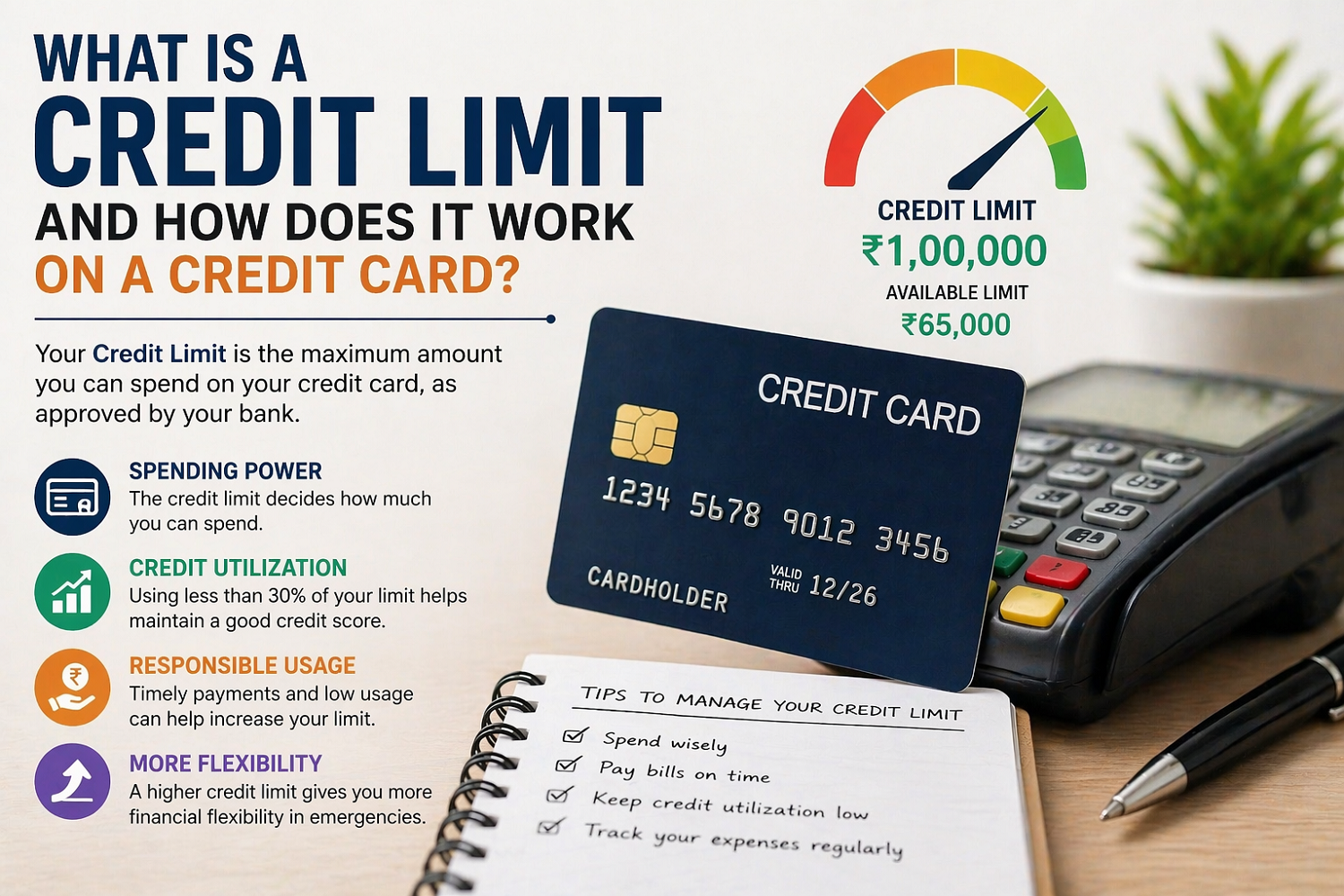

What Does Credit Limit Actually Mean?

A credit limit does not mean any extra income. It is actually a borrowing cap set by the bank.

For instance, your card has a credit limit of ₹100,000. That means you can spend maximum ₹100,000 within the fixed given period.

Now comes the most crucial part. As per the common rule, you can’t exceed the given limit. That means you cannot make further transactions once you reach the approved maximum limit. Moreover, you can again start your transactions after repaying the outstanding balance.

Importantly, this limit is applicable across all types of transactions. This includes shopping, bill payments, and cash withdrawals (if enabled).

It is necessary to understand that cash withdrawals may also have a separate sub-limit. And it must be within the overall given credit limit.

How Banks Decide Your Credit Limit

Banks determine your credit limit after evaluating several notable factors.

The first and most important factor is your monthly income. It reflects your repayment ability. Apart from this, the other salient factors are your credit score, existing debts, and your employment stability.

One essential fact is you can receive a higher credit limit if you have a strong credit history and a high income. New users and people with limited credit history often get a lower limit initially.

The Importance of Credit Limit

A credit limit does not just signify spending capacity. It directly impacts your credit utilisation ratio. Notably, the utilisation ratio is the percentage of your limit that you are allowed to use.

For example, your credit limit is ₹100,000, and you have used ₹50,000. That means your utilisation is 50%. Now, instead of 50%, if you can keep your usage below 30–40% of your credit limit, then it is generally considered healthy.

In truth, high utilisation can impact your credit score negatively, even if you pay your bills on time.

Can Your Credit Limit Be Increased?

Yes, a credit limit can be increased, and banks may enhance the limit over time. However, there are two prime factors, i.e., your usage and repayment behaviour, which decide this expansion.

If you always pay your bills on time and simultaneously use your card responsibly, then you may receive an automatic limit enhancement. Also, you can request a limit increase manually by providing your updated income proof.

Nonetheless, it must be better if you first become confident about managing a higher limit responsibly, and then you should apply for limit enhancement.

Things to Keep in Mind

You can find more flexibility with a higher credit limit. However, a higher limit can also lead to overspending if you cannot manage it carefully.

Therefore, to avoid such a situation, you need to always track your expenses and simultaneously avoid using your full limit unless it is absolutely necessary.

One crucial fact is exceeding the credit limit may result in penalties and additional charges. A few banks may allow over-limit transactions, but they usually come with fees.

Conclusion

It is extremely important to understand the credit limit rightly in order to continue responsible credit card usage.

Responsible usage controls how much you can spend. It also influences your credit score and financial discipline.

Now, the important part is you can use your credit card to earn maximum benefits without becoming the debt victim. And it is possible if you use your credit limit wisely and continue your spending consciously for future gain.